Taxation is a fundamental aspect of every country’s economic structure, serving as a primary source of revenue for the government to fund infrastructure, education, healthcare, defense, and public welfare programs. In India, taxes are broadly classified into two categories — direct taxes and indirect taxes. Understanding the distinction between these two is essential for taxpayers, professionals, and students alike.

What Are Direct Taxes?

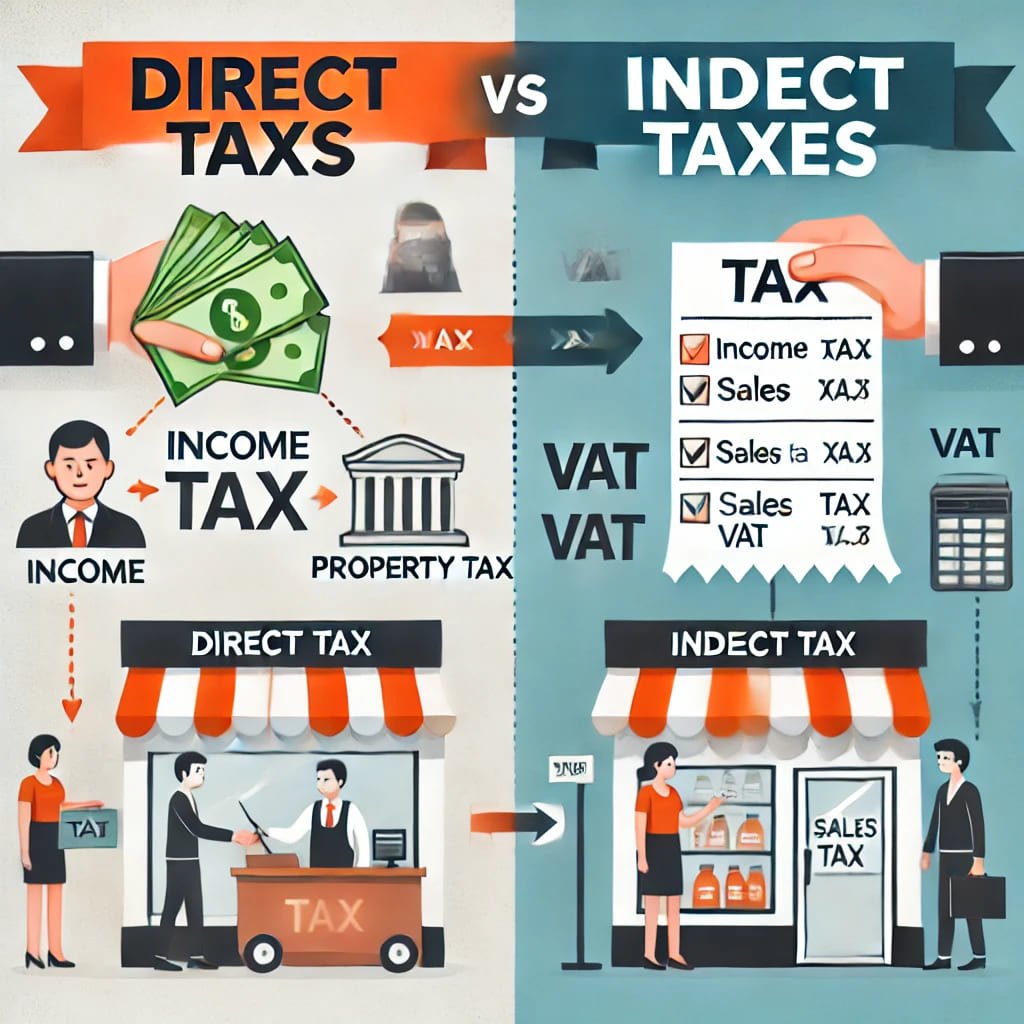

Direct taxes are taxes that are imposed directly on an individual or an entity and are paid directly to the government. The responsibility of paying the tax cannot be shifted to another person. Some of the most common types of direct taxes in India include:

- Income Tax: Paid by individuals and entities on their income or profits.

- Corporate Tax: Levied on the profits of companies.

- Capital Gains Tax: Charged on the profit earned from the sale of capital assets.

- Wealth Tax: Though abolished in 2015, it was earlier imposed on the net wealth of individuals and companies.

A significant feature of direct taxes is that they are progressive in nature, i.e., higher the income, higher the rate of tax.

What Are Indirect Taxes?

In contrast, indirect taxes are levied on goods and services rather than on income or profits. These taxes are collected by intermediaries (like manufacturers, sellers, or service providers) and passed on to the government. The burden of tax is ultimately borne by the consumer. Major examples include:

- Goods and Services Tax (GST): A comprehensive indirect tax that has subsumed most previous indirect taxes like VAT, excise duty, and service tax.

- Customs Duty: Levied on goods imported into or exported out of the country.

- Excise Duty: Imposed on the manufacture of goods within the country (largely merged into GST for most goods).

Indirect taxes are generally regressive in nature, affecting all consumers uniformly regardless of their economic status.

📊 Infographic: Direct vs. Indirect Taxes

| Feature | 🧾 Direct Taxes | 🛒 Indirect Taxes |

|---|---|---|

| Definition | Tax paid directly by individuals or organizations to the government. | Tax collected by intermediaries and passed on to the government. |

| Examples | Income Tax, Corporate Tax, Capital Gains Tax | GST, Customs Duty, Excise Duty |

| Tax Burden | Cannot be shifted; borne by the taxpayer | Shifted to consumers; included in product prices |

| Administration | Managed by CBDT (Central Board of Direct Taxes) | Managed by CBIC (Central Board of Indirect Taxes & Customs) |

| Nature | Progressive (higher income = higher tax rate) | Regressive (same rate for all, affects poor more) |

| Compliance | Requires self-declaration and filing returns | Automatically collected at point of sale |

| Tax Base | Based on income or wealth | Based on consumption or transactions |

| Evasion vs. Avoidance | Harder to evade due to traceability | Evasion possible through informal trade |

| Impact on Inflation | No direct impact | Can contribute to price rise |

Importance in India’s Tax Framework

India’s tax system relies heavily on both direct and indirect taxes to ensure fiscal sustainability. The Central Board of Direct Taxes (CBDT) oversees the administration of direct taxes, while the Central Board of Indirect Taxes and Customs (CBIC) manages indirect taxes.

The shift to GST in 2017 marked a significant reform in indirect taxation, streamlining multiple taxes into a single system, promoting ease of doing business, and increasing transparency. On the other hand, the government continues to refine the direct tax system through measures like the faceless assessment scheme, advance rulings, and digital filing mechanisms.

Conclusion

Both direct and indirect taxes play complementary roles in the Indian economy. While direct taxes promote equity and redistribute wealth, indirect taxes ensure that revenue is generated from consumption and trade activities. Understanding the nuances of each not only helps in better financial planning for individuals and businesses but also fosters greater tax compliance and participation in nation-building.