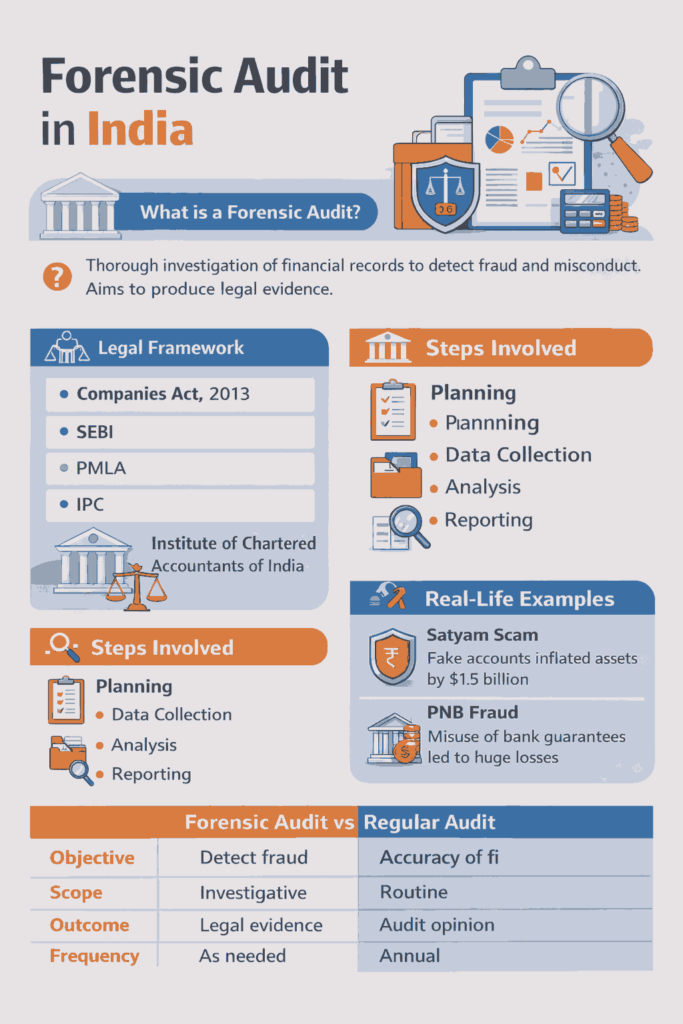

What is a Forensic Audit?

A forensic audit is a detailed examination of financial records to detect fraud, misconduct, or financial irregularities. Unlike a regular audit, it is conducted with the intention of producing evidence that can be used in a court of law.

It combines concepts from:

- Accounting

- Auditing

- Law

Simply put, if a regular audit checks whether financial statements are accurate, a forensic audit investigates whether fraud or misconduct may have occurred (in simple words to check if there is any fraud or cheating occurred).

Why is Forensic Audit Important in India?

India has witnessed several high-profile corporate frauds that shook public confidence. Cases like the Satyam scandal highlighted the urgent need for stronger financial investigation mechanisms.

Today, forensic audits are crucial for:

- Detecting corporate fraud

- Supporting legal proceedings

- Ensuring transparency and accountability

- Protecting investors and stakeholders

Businesses should consider a forensic audit in situations such as:

- Suspicion of fraud or financial irregularities

- Disputes between partners or shareholders

- Whistleblower complaints

- Unexplained losses or cash flow issues

- Regulatory notices or investigations

Legal Framework for Forensic Audits in India

Forensic audits in India are guided by various laws and regulatory bodies:

Companies Act, 2013

- Empowers authorities to order investigations into company affairs

- Sections like 210–212 deal with investigation by government agencies

SEBI (Securities and Exchange Board of India)

- Listed companies may be directed to conduct forensic audits in case of suspected fraud

- Ensures investor protection

Institute of Chartered Accountants of India

- Provides guidance and training for chartered accountants

- Offers certifications in forensic accounting and fraud detection

Other Relevant Laws

- Prevention of Money Laundering Act (PMLA)

- Indian Penal Code (IPC)

- Information Technology Act, 2000

Types of Forensic Audits

1. Fraud Investigation

Focuses on uncovering:

- Embezzlement

- Fake invoices

- Misuse of company funds

2. Litigation Support

Helps in legal disputes such as:

- Shareholder disagreements

- Contract breaches

3. Corporate Misconduct

Investigates unethical practices by employees or management

4. Regulatory Investigations

Triggered by authorities like SEBI or banks

How Does a Forensic Audit Work?

Here’s a simple step-by-step breakdown:

1. Planning

- Define scope and objectives

- Identify suspicious areas

2. Data Collection

- Financial statements

- Emails, invoices, contracts

3. Analysis

- Identify unusual patterns

- Use data analytics tools

4. Reporting

- Prepare a clear, evidence-based report

5. Legal Support

- Findings may be presented in court

Techniques Used in Forensic Auditing

- Data analytics and trend analysis

- Ratio analysis

- Digital forensics

- Background checks

- Interviews and information gathering

These techniques help auditors “connect the dots” and uncover hidden fraud.

Forensic Audit vs Regular Audit

| Aspect | Regular Audit | Forensic Audit |

| Objective | Accuracy of financial statements | Detect fraud |

| Scope | Routine | Investigative |

| Outcome | Audit opinion | Legal evidence |

| Frequency | Annual | As needed |

Real-World Examples from India

Satyam Computer Services

In 2009, the chairman of Satyam Computer Services confessed to a $1.5 billion fraud.

- The Scheme: The company inflated its cash balances by creating thousands of fake bank statements and invoices. They essentially showed “money in the bank” that didn’t exist to keep their stock price high.

- The Catch: Forensic investigators compared the company’s internal records with independent confirmations from banks. When the banks couldn’t find the accounts Satyam claimed to have, the house of cards collapsed.

Punjab National Bank Fraud Case

This involved the misuse of the SWIFT (international messaging system for banks) network.

- The Scheme: Bank officials issued “Letters of Undertaking” (a type of guarantee) without recording them in the bank’s core system. This allowed the perpetrators to get loans from overseas branches of other banks using PNB’s credit.

- The Catch: Forensic auditors tracked the audit trail of the SWIFT messages. Even though the transactions weren’t in the accounting ledger, the digital trail of the messages sent to other banks was permanent and undeniable.

Skills Required to Become a Forensic Auditor

If you’re interested in this field, here are key skills you’ll need:

- Strong analytical thinking

- Knowledge of Forensic Accounting / Auditing

- Understanding of Indian laws and regulations

- Attention to detail

- Communication and reporting skills

“Who” can become a forensic auditor generally falls into three categories:

- Chartered Accountants (CAs): The most preferred candidates. Most high-stakes forensic audits mandated by the RBI or SEBI require a CA to lead.

- Company Secretaries (CS) & Cost Accountants (CMA): Often hired for compliance-heavy investigations or internal vigilance roles.

- Finance Professionals (MBA/M.Com): Can enter the field by focusing on Financial Risk Management (FRM) and data analytics, typically starting in the “Risk Advisory” arms of major firms.

Future Scope of Forensic Auditing in India

With the rise of digital payments, startups, and online transactions, financial fraud is becoming more sophisticated. This has increased the demand for forensic auditors in areas like:

- Cybercrime investigations

- Blockchain analysis

- Financial fraud detection

Forensic auditing is no longer optional — it’s becoming a necessity in modern business.

Final Thoughts

Forensic audits act as a financial detective, uncovering the truth behind complex transactions. In a rapidly growing economy like India, they play a vital role in maintaining trust, transparency, and accountability.

Whether you’re a student, finance professional, or business owner, understanding forensic auditing can give you valuable insights into how financial fraud is detected and prevented.

Need assistance with forensic audit or fraud investigation?

We assist businesses in identifying financial irregularities, strengthening internal controls, and supporting legal proceedings with evidence-based reports.

Author

Mr. Ayush Dev

Intern

Pavan Goyal and Associates (Chartered Accountants)

Office No. B212, GO Square, Mankar Chowk, Wakad, Pune 411057

Email – office@goyalca.com

Contact – 9762763351