Selling a property can result in significant profits—but it also brings tax implications. Understanding capital gains tax in India is essential to ensure proper compliance and effective tax planning.

This guide explains everything in simple terms, along with practical strategies to reduce tax liability.

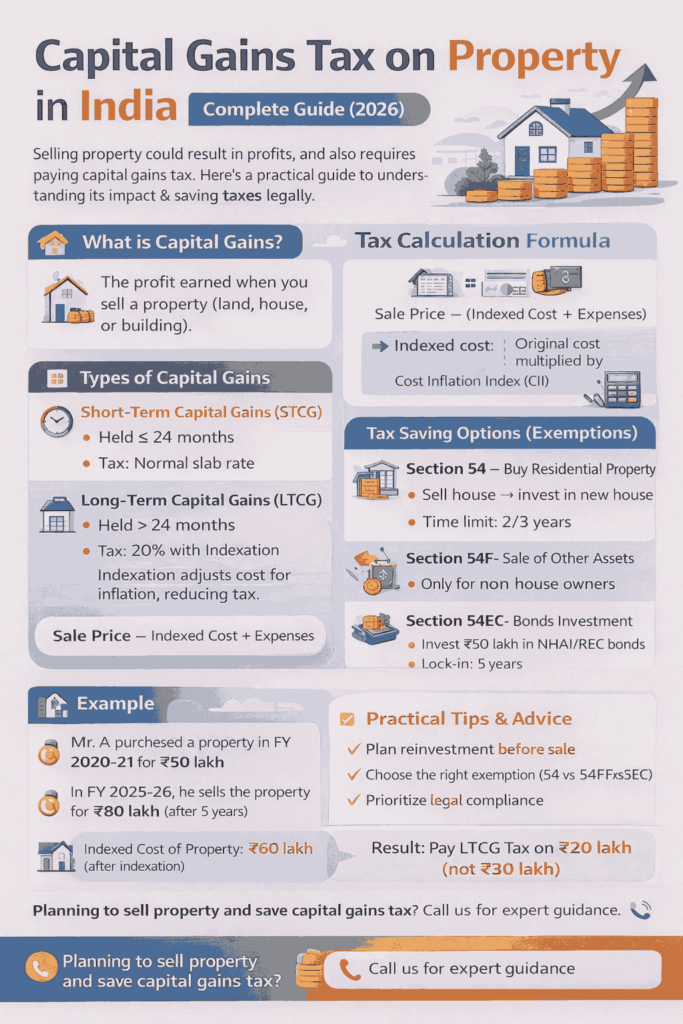

What is Capital Gains on Property?

When you sell a property (land, house, or building) at a profit, the gain is called capital gain and is taxable under the Income Tax Act

Types of Capital Gains

1. Short-Term Capital Gains (STCG)

- Property held for ≤ 24 months

- Taxed as per normal income tax slab

2. Long-Term Capital Gains (LTCG)

- Property held for > 24 months

- Generally taxed at:

- 20% with indexation (most common method)

👉 Indexation reduces tax by adjusting cost for inflation.

How Capital Gains is Calculated

Basic Formula:

Capital Gain = Sale Price – (Indexed Cost of Purchase + Expenses)

- Indexed cost adjusts original purchase price using Cost Inflation Index (CII)

- Reduces taxable gain significantly

💡 Example (Simple Understanding)

Mr. A purchased a property for ₹50 lakh and sold it after 5 years for ₹80 lakh.

After applying indexation, the cost increases (say ₹65 lakh), and taxable gain reduces to ₹15 lakh instead of ₹30 lakh.

👉 Result: Lower tax liability due to indexation

Exemptions Available (Tax Saving Options)

🔹 Section 54 – Reinvestment in Residential Property

- Applicable on sale of residential house

- Invest in another house:

- Within 2 years (purchase) OR

- Within 3 years (construction)

- Exemption allowed up to ₹10 crore capital gain

👉 Option to invest in 2 houses (once in lifetime) if gain ≤ ₹2 crore

🔹 Section 54F – Sale of Other Assets (Other than residential house)

- Applicable when asset sold is not residential house

- Must invest full sale consideration in a residential property

Key Conditions:

- Must not own more than 1 house (with conditions)

- Proportionate exemption if partial investment

🔹 Section 54EC – Investment in Bonds

- Invest in specified bonds (NHAI/REC)

- Time limit: 6 months

- Maximum investment: ₹50 lakh

- Lock-in period: 5 years

👉 Safe option for conservative taxpayers

⚠️ Important Practical Points

- If exemption is not utilised before return filing → deposit in Capital Gains Account Scheme (CGAS)

- New property should not be sold within 3 years

- Documentation is critical for claiming exemptions

📉 Real-Life Example (Exemption)

Ms. B sold a house and earned ₹30 lakh capital gain. She reinvested in another residential property within 2 years.

👉 Result: Full exemption under Section 54 → No capital gains tax payable

📈 Property Tax Planning Tips

✔ Plan reinvestment before sale

✔ Use indexation effectively

✔ Choose correct exemption (54 vs 54F vs 54EC)

✔ Maintain proper documentation

✔ Evaluate timing of sale

📌 Conclusion

Capital gains tax on property is a crucial aspect of financial planning. With proper understanding of tax rules, exemptions, and timing, taxpayers can significantly reduce their tax liability.

Early planning and professional guidance can help you make the most of available benefits.

📞 Need Help with Capital Gains Tax Planning?

Planning to sell property and want to minimise tax liability?

We assist with:

- Capital gains computation

- Tax-saving strategies

- Exemption planning

- Compliance and documentation

👉 Contact us for a personalised consultation.

⚠️ Disclaimer

This article is for general informational purposes only and should not be considered professional advice. Please consult a qualified professional before taking any action.

Author

Ms. Shravani Nikum

Intern

Pavan Goyal and Associates (Chartered Accountants)

Office No. B212, GO Square, Mankar Chowk, Wakad, Pune 411057

Email – office@goyalca.com

Contact – 9762763351