Being aware of the risks associated with an investment can help investors make better decisions and avoid potential pitfalls.

By understanding the different types of risk including Inflation risk, investors can create a more balanced portfolio, reducing the impact of adverse market events and increasing the likelihood of achieving their financial goals.

It is possible and prudent to manage inflation risks by understanding the basics of risk and how it is measured. Learning the risks that can apply to different scenarios and some of the ways to manage them holistically will help all types of investors and business managers to avoid unnecessary and costly losses.

“In this post, we’ll explore how inflation affects budgeting, investments, borrowing, and more—plus how to manage finances smartly in an inflationary environment & how to mitigate impact of inflation on Financial Management / Finances”.

What is Inflation

Inflation is defined as the rate at which the general level of prices for goods and services rises, diminishing the purchasing power of people. As prices rise, each rupee buys fewer goods and services.

Central banks, such as the Federal Reserve in the United States or Reserve Bank of India, often aim for a moderate inflation rate (around 2%) as a sign of a healthy economy. However, when inflation surges unexpectedly, it can disrupt financial planning.

Inflation trends in the current economic climate

In the year of 2024, inflation rates have fluctuated significantly due to factors such as the COVID-19 pandemic, supply chain disruptions, and geopolitical tensions including wars / conflicts between nations. According to the Bureau of Labour Statistics, inflation rate in India hit a peak of 6.7% in the year 2022, the highest in over four decades. These fluctuations illustrate the volatility of inflation and highlight the importance of flexible financial management strategies. Historically, the inflation in India has fluctuated between 3.40% to 6.70%.

How Inflation impacts Financial management

“Have you noticed your grocery bill increasing up lately? That’s inflation in action—and it doesn’t just affect our wallets, but the entire financial management landscape.”

Inflation affects nearly every aspect of financial decision-making—whether you’re managing a household budget, a corporate finance department, or a national treasury. Let’s break down the key areas impacted by inflation, with real-world examples to make it crystal clear.

1. Decreased Purchasing Power

What it means:

Inflation reduces the value of money over time. As prices rise, each rupees buys fewer goods and services. This impacts both consumers and businesses.

Example:

A company that spent ₹ 100,000 a year ago to purchase raw materials now needs ₹ 105,000 for the same quantity, assuming a 5% inflation rate. If revenue hasn’t increased at the same pace, profit margins shrink.

2. Budgeting and Forecasting Becomes Uncertain

What it means:

Inflation makes it hard to predict future costs. This leads to challenges in long-term financial planning, especially for fixed-income projects or long-term contracts.

Example:

A construction firm bidding on a two-year project may underestimate future costs of steel and labour. If inflation spikes during that time, their initial budget may fall short, leading to losses unless there’s an inflation-adjustment clause.

3. Higher Cost of Capital

What it means:

Central banks often raise interest rates to combat inflation. This makes borrowing more expensive for businesses and individuals.

Example:

In 2022–2023, the Reserve Bank of India hiked interest rates aggressively to curb inflation. As a result, corporate borrowing costs soared. Tech companies that relied on cheap loans for expansion had to scale back, lay off staff, or halt R&D investments.

4. Changing Investment Strategies

What it means:

Inflation affects how investors allocate assets. Fixed-income investments (like bonds) lose value during inflation unless they are inflation-protected. Stocks, real estate, and commodities often perform better.

Example:

Due to rising inflation eroding returns from bank fixed deposits, Rajesh from Mumbai shifted part of his savings to equity mutual funds and gold ETFs to preserve and grow his wealth. This change helped him beat inflation and improve long-term financial planning.

5. Impact on Financial Reporting and Profit Margins

What it means:

Companies face rising operating costs (materials, wages, utilities). If they can’t raise prices proportionally, profit margins decline. Also, inflation can distort financial statements if historical costs aren’t adjusted.Example:

A manufacturing company may report the same revenue year over year, but rising raw material and energy costs erode net income. In economies with hyperinflation (e.g. Venezuela – source google), financial reports can become meaningless without adjustments.

6. Inventory and Supply Chain Management

What it means:

Inflation affects the cost and availability of supplies. Businesses may need to bulk-buy inventory or renegotiate contracts to lock in lower prices, impacting working capital.

Example:

Retailers like Walmart and Target, during post-COVID supply chain disruptions, had to adjust inventory strategies. They faced inflated shipping costs, forcing them to revise supply chain models and pricing strategies.

Case Study – 1

If an investment earns a 4% return but inflation is 5%, the real return on the investment is -1%, resulting in a loss of purchasing power.

Inflation risks reduce the real value of money over time as the prices of goods and services steadily rise in an economy as the years go by.

Conclusion: Always plan to save for the future cost, not today’s price. And if possible, invest your savings where your returns are higher than the inflation.

Case Study – 2 – Mr. Verma – A Teacher Saving for Child’s Education

Age: 35 (Retire after 15 year).

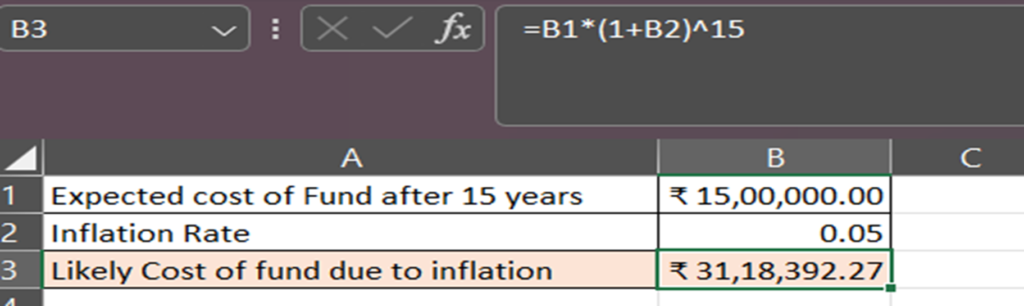

Goal: Save ₹ 15 lakhs in 15 years to fund his child’s college education

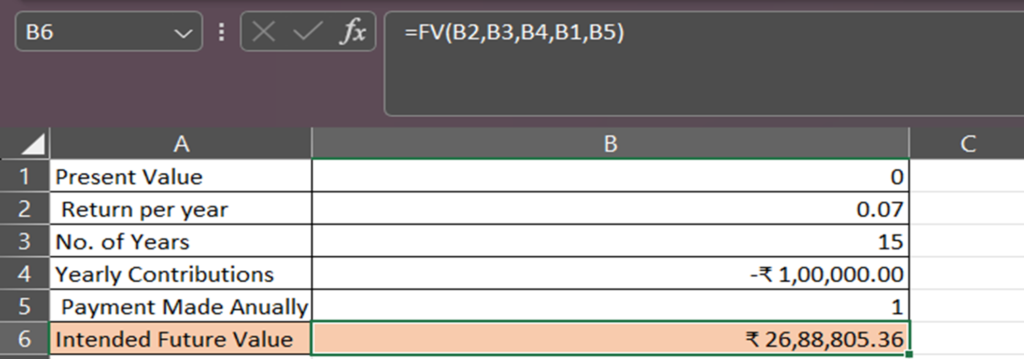

Annual Investment: ₹ 1,00,000

Present Value: ₹ 0

Return Assumption: 7% annually (from low-risk instruments like debt funds or PPF) Inflation Rate: 5% (college costs rise each year)

Step 1: Adjust the Target for Inflation

If college costs rise at 5% annually, the inflated future cost will be:

Use this formula – Present value = Future Cost*(1+ inflation rate)^years

So, instead of saving ₹ 15 lakhs, Mr. Verma now needs ₹ 31,18,392.27 in 15 years due to inflation.

Step 2: Check If Current Savings Plan Is Enough:

This will return: ₹ 26,88,805.36

Shortfall: He’ll only accumulate ₹ 26,88,805.36, but needs ₹ 31,18,392.27

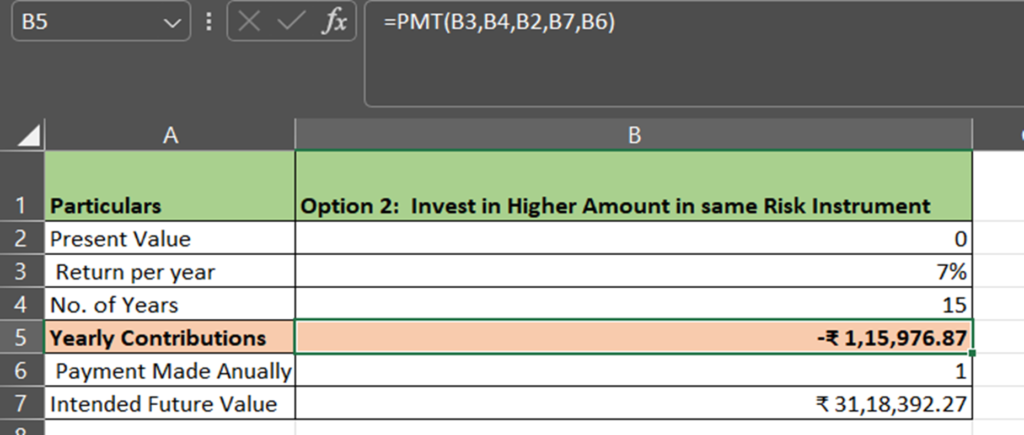

Options Mr. Verma Has:

- Invest in higher-return assets

Try investing in equity mutual funds or hybrid funds giving 9% returns. - Increase annual investment

What annual investment will grow to ₹ 31,18,392.27 at 7% in 15 years?

Result: ₹ 1,15,976.87/year (instead of ₹ 1,00,000)

Conclusion:

- Due to inflation, Mr. Verma needs to pay more than, what he originally planned.

- To reach that inflated goal, he must either invest more money or choose higher-return (riskier) investments.

How to Mitigate Impact of inflation on Financial Management

- Invest in Inflation-Linked Assets (E.g. Inflation-Indexed Bonds issued by the Indian government)

- Diversify into Equities

- Invest in Exchange Traded Funds (ETF’s)

- Increase Contributions Regularly (Increase your investments by 5–10% annually)

- Use Tax-Advantaged Instruments

- Avoid staying fully invested into Long-Term Fixed Returns (Without Inflation Link)

- Regularly Review and Rebalance Portfolio

Thus, when faced with inflation-driven cost increases; successful financial management means controlling costs aggressively, finding efficiencies, and carefully adjusting prices — not just sitting back and hoping for the best.

Author

Ms. Diksha Gupta

Article Intern

Pavan Goyal and Associates (Chartered Accountants)

Office No. B212, GO Square, Mankar Chowk, Wakad, Pune 411057

Email – office@goyalca.com

Contact – 9762763351